A tale of three scopes: Part 2

In addition to scope 1 (direct emissions) and scope 2 (purchased electricity, heat, and steam), many organizations now have scope 3 emissions reduction targets in their climate change strategies. This life cycle approach not only helps identify scope 3 decarbonization opportunities by defining the necessary strategies, tools, and support needed at an organizational level, but also promotes unprecedented collaboration and innovation along critical value chains necessary for the energy transition.

What is the significance of scope 3 emissions to extractive resource companies?

Extractive resource companies have recognized the importance of scope 3 greenhouse gas (GHG) emissions to their overall climate change strategy, with leading organizations leveraging scope 3 strategies to optimize their value chain, reduce costs and emissions, and advance resiliency throughout their own operations and their partners’ operations.

Nearly half of leading metals companies have a scope 3 reduction target, and the next step is to identify an approach to reducing emissions and considering scope 3 in business decision-making. With this in mind, promoting collaboration and fostering innovation across their value chain is essential. The necessary experience and expertise across these value chains provides insight and fosters connections, generating real value for our clients, their suppliers, and their customers.

What position should organizations take to address scope 3 emissions?

Planning for and identifying reductions can be challenging. With variabilities surrounding market dynamics and feed and product requirements, the emissions of value chain partners may not always be straightforward.

The value chains of finished materials begin with raw materials produced by extractive resource companies, who pass their emissions to successive customers downstream. These organizations can shape markets, promote low carbon products, and transform global value chains to reduce GHG emissions.

An organization’s scope 3 reduction program must be informed by their organizational capabilities and focus, along with their market position and stakeholder requirements. Conditional to these factors, organizations may embark on various levels of engagement within their value chain and—as outlined below—can position themselves as a hesitator, follower, leader, or shaper within their scope 3 action plan.

Hesitators |

Followers |

Leaders |

Shapers |

|

|---|---|---|---|---|

| Supply Chain Engagement |

|

|

|

|

| Product and Market Positioning |

|

|

|

|

| Direct Reductions |

|

|

|

|

Considering a company’s position, action plans can then be developed that include:

- Supply chain engagement: collaborating with suppliers, customers, and travel providers.

- Product and market positioning: improve market position by producing a lower carbon product as a competitive advantage.

- Direct reductions: reducing direct emissions in operations that consequently reduce scope 3 emissions (e.g., reducing fuel consumption, using lower carbon intensity fuels, or switching to renewable energy).

As with strategies to reduce scope 1 and 2 emissions, scope 3 strategies are bespoke to an organization. By first identifying organizational objectives and emissions drivers, organizations can determine how they can best engage with their value chain and the opportunities that unlock the most value.

What initiatives should organizations pursue to decarbonize value chain emissions?

Opportunities to partner with suppliers and customers can leverage synergies through mutually beneficial solutions as outlined in the graphic below. Organizations can also incorporate scope 3 considerations into designing processes and selecting operational sites. Factors such as proximity to suppliers and customers; availability of and proximity to low carbon energy sources; employee commuting and travel; circularity of products at end-of-life; and waste generation when designing processes and selecting operational sites should be considered.

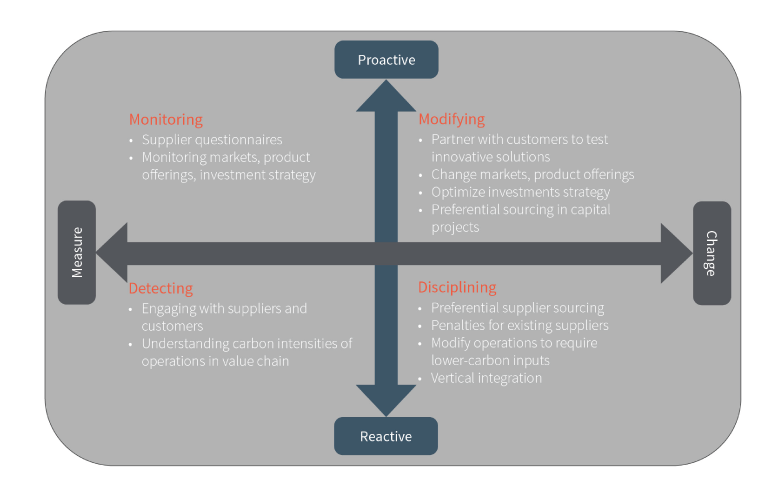

Scope 3 emissions abatement opportunities are classified by avoiding emissions (proactive) or addressing existing emissions (reactive). The matrix below maps an organization’s strategy to actionable items by considering scope 3 reduction initiatives and integration.

Depending on the level of engagement with their supply chain and industry position, organizations can develop an actionable and coordinated approach to achieving their scope 3 targets.

How can Hatch partner with organizations in creating and achieving scope 3 goals?

Hatch has partnered with clients to develop and execute scope 3 strategies that diversify offerings, build resilience, and reduce emissions across value chains and commodities. Specifically, Hatch can help our clients by:

- Identifying, quantifying, and implementing scope 3 reduction opportunities.

- Engaging with suppliers and customers to understand their GHG footprints.

- Optimizing internal value chains to promote low carbon products.

- Incorporating scope 3 considerations into business decisions (e.g., site selection, suppliers, customers, circularity, brownfield vs. greenfield).

- Identifying markets for low-carbon products.

- Assessing the impact of alternate processes and products on value chain emissions.

Scope 3 emissions and corresponding reduction strategies will increasingly become a part of climate change and decarbonization discussions. As a leader in climate change mitigation and adaptation, Hatch is well positioned to support your organization on this journey.

Matthew Tutty

EIT | Climate Change and Sustainability, Climate Change Business Practice

Matthew is an Engineer-in-Training with expertise in climate change. He has broad experience across various aspects of developing climate change strategy including quantifying emissions inventories, climate-related risk analysis, and identifying greenhouse gas emission reduction opportunities. Matthew has worked with many key metals accounts to define strategies to achieve their decarbonization goals.

Recent work Matthew has been involved in includes developing product carbon intensity calculation methodologies for the base and precious metals products and quantifying at a concept-level and early engineering stage decarbonization opportunities. Matthew’s dedication to community development was recognized with the Engineers’ Canada Gold Medal Student Award in 2021 which recognizes the exceptional achievements of an undergraduate engineering student who has demonstrated leadership, resiliency, and positive impact in their engineering studies and community.